![[Solved] How Do You Pay Back a Reverse Mortgage?](/_next/image?url=https%3A%2F%2Fdynamic-light-ab6e2536d6.media.strapiapp.com%2Fpay_back_a_reverse_mortgage_964a6e43d3.png&w=3840&q=75)

[Solved] How Do You Pay Back a Reverse Mortgage?

Facing a reverse mortgage that's due can feel overwhelming, whether you're a borrower wanting to exit the loan or an heir handling an estate. I completely understand the anxiety around protecting family wealth.

The good news? You have several distinct options, and you won't have to drain your personal savings to settle it. This guide walks you through exactly how to pay back a reverse mortgage, empowering you to make the right financial move without panic.

Key Takeaways

-

Non-recourse protection: Federal rules guarantee you or your heirs will never owe more than the home's current value.

-

Multiple repayment paths: You can sell the property, refinance, use cash, or hand the keys back to the lender.

-

The 95% rule: Heirs or the estate may satisfy a due-and-payable HECM by paying the lesser of the loan balance or 95% of the home's appraised value, subject to HUD's applicable rules.

-

Timeframe: Families typically have about six months to resolve the loan after the borrower dies, and may be able to request extensions that can extend the timeline up to 12 months.

How Does a Reverse Mortgage Balance Grow?

Before diving into repayment, I always remind clients to grasp why their balance has increased so much. Most reverse mortgages in the US are Home Equity Conversion Mortgages (HECMs). With an HECM, you aren't making monthly principal and interest payments. Instead, the lender adds the interest, mortgage insurance premiums, and fees to your outstanding balance every single month.

Because of compounding interest, meaning you pay interest on the interest, the amount you owe grows significantly over time while your home equity shrinks. Understanding this snowball effect is crucial when deciding if you should sell the property or try to pay off the debt out of pocket.

Also Read:

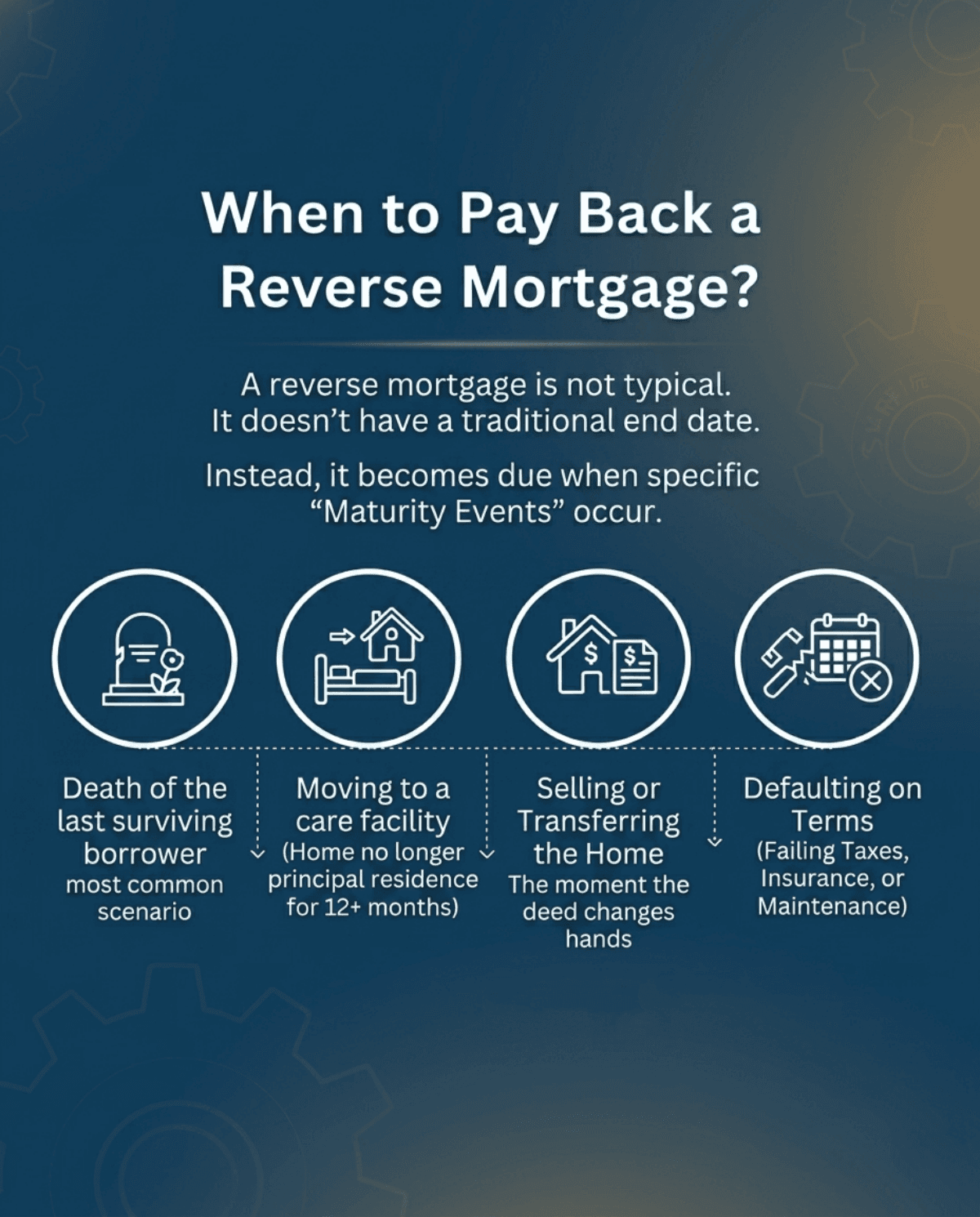

When to Pay Back a Reverse Mortgage?

A reverse mortgage isn't a typical loan. It doesn't have a traditional end date. Instead, it becomes due and payable when specific "maturity events" occur. Usually, it happens when you permanently leave the house.

Here are the main triggers that force repayment:

-

Death of the last surviving borrower: This is the most common scenario, leaving the responsibility to the estate or heirs.

-

Moving to a care facility: If the home is no longer your principal residence and you remain in a healthcare facility for more than 12 consecutive months, the loan may become due and payable unless a co-borrower or eligible non-borrowing spouse still lives in the home.

-

Selling or transferring the home: The moment the deed changes hands, the balance is due.

-

Defaulting on terms: Failing to pay property taxes, maintain homeowners insurance, or keep the home in good repair can cause the loan to become due and payable and may lead to foreclosure.

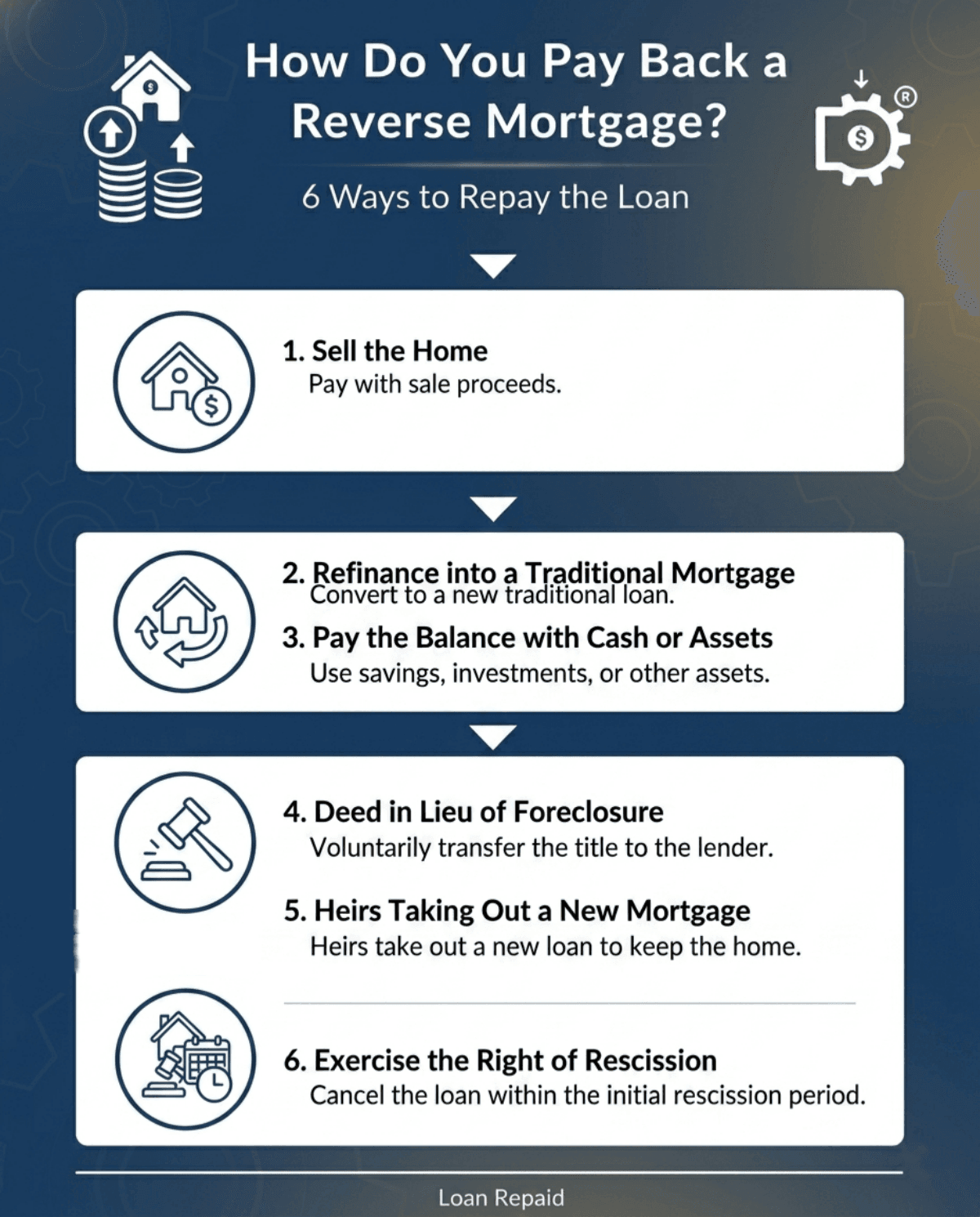

How Do You Pay Back a Reverse Mortgage?

The best exit strategy depends entirely on your current home equity and whether your ultimate goal is keeping the property within the family or simply walking away clean. Let's explore your main choices.

1. Sell the Home

Selling the property is the most frequent way I see families resolve this debt. If the real estate market has been kind and your home's value exceeds the loan balance, you sell the house, pay off the lender, and pocket the remaining equity.

But what if the balance is higher than the home's worth? Don't panic. HECMs are non-recourse loans. This means neither you nor your heirs are personally liable for the shortfall. If you sell the home for its fair market value, the proceeds go to the lender, and the FHA mortgage insurance fund covers the rest. Your personal assets, retirement accounts, or other inherited wealth remain completely untouched.

2. Refinance into a Traditional Mortgage

Sometimes, borrowers realize they want to leave a debt-free house to their kids or simply dislike the rapidly compounding interest. If you want to switch gears, you can refinance the reverse mortgage into a conventional forward mortgage.

I usually caution that this route requires you to meet strict lending standards. You must demonstrate sufficient income, carry a manageable debt-to-income (DTI) ratio, and have a solid credit score to qualify. Essentially, you're taking out a brand-new loan to wash away the old one. Once approved, you'll start making regular monthly principal and interest payments. It's a great move if your financial situation has improved since you originally took out the HECM.

Also Read:

3. Pay the Balance with Cash or Assets

If preserving the family home is an emotional priority and you have high liquidity, using cash or liquid assets to wipe out the debt is a viable choice.

This is where the incredible "95% Rule" comes into play, a detail I always ensure heirs know about. Under HUD regulations, if the loan is completely underwater (you owe more than the house is worth), you don't have to pay the full bloated balance. Heirs can purchase the property outright for just 95% of its current appraised value. The FHA absorbs the remaining loss. It's an incredibly powerful consumer protection that allows families to keep their childhood home safely.

4. Deed in Lieu of Foreclosure

Dealing with real estate can be exhausting, especially during the grieving process. If the property is severely underwater, needs extensive repairs, or the heirs simply don't want the hassle of listing it on the market, you can execute a "Deed in Lieu of Foreclosure."

In layman's terms, you are voluntarily handing the keys and the property deed back to the loan servicer. They take legal ownership and assume the burden of selling it. Because HECMs are non-recourse loans, a deed in lieu of foreclosure can be used to satisfy the debt, subject to the servicer's and HUD's requirements. It allows the estate to walk away cleanly, and most importantly, it does not negatively impact the heirs' personal credit scores.

5. Heirs Taking Out a New Mortgage

What if your children want to keep the family home but don't have hundreds of thousands of dollars in cash lying around? They can take out a new traditional mortgage in their own names to buy the property from the estate.

The funds from this new loan are used to pay off the reverse mortgage servicer. If the loan is due and payable, HUD rules may allow the property to be retained or satisfied for the lesser of the loan balance or 95% of the appraised value. The heirs will only need to finance up to 95% of the current market value if the original loan balance is higher. However, they must independently qualify for this new mortgage based on their own creditworthiness and income levels.

6. Exercise the Right of Rescission

I occasionally get frantic calls from clients who just signed their closing documents and immediately regret it. If you act quickly, you have an emergency parachute: the Right of Rescission.

Federal law grants you a strict three-business-day window to cancel the transaction after closing. This right generally applies to certain mortgage transactions secured by your principal residence, including most reverse mortgages, and the three-business-day clock starts only after the required disclosures and rescission notices are delivered.

To exercise this right, you must notify the lender in writing before midnight of the third business day. If done correctly, the lender must refund any fees you paid, and the loan is voided without penalty. Remember, this is a very brief grace period, not a long-term strategy.

Should You Get Out of a Reverse Mortgage?

Deciding to exit a reverse mortgage before a maturity event happens requires careful financial calculus. I recommend weighing these factors before making a move:

-

Current interest rates: Are conventional mortgage rates significantly lower than your current compounding rate?

-

Cash flow: Can you realistically afford traditional monthly mortgage payments without straining your retirement budget?

-

Future living plans: Do you plan to downsize or move into a care facility within the next few years? If so, paying massive closing costs to refinance now might be a waste of money.

Disclaimer: I strongly advise consulting with a HUD-approved housing counselor or a fiduciary financial advisor. Every homeowner's equity position is unique, and professional guidance is essential before altering your setup.

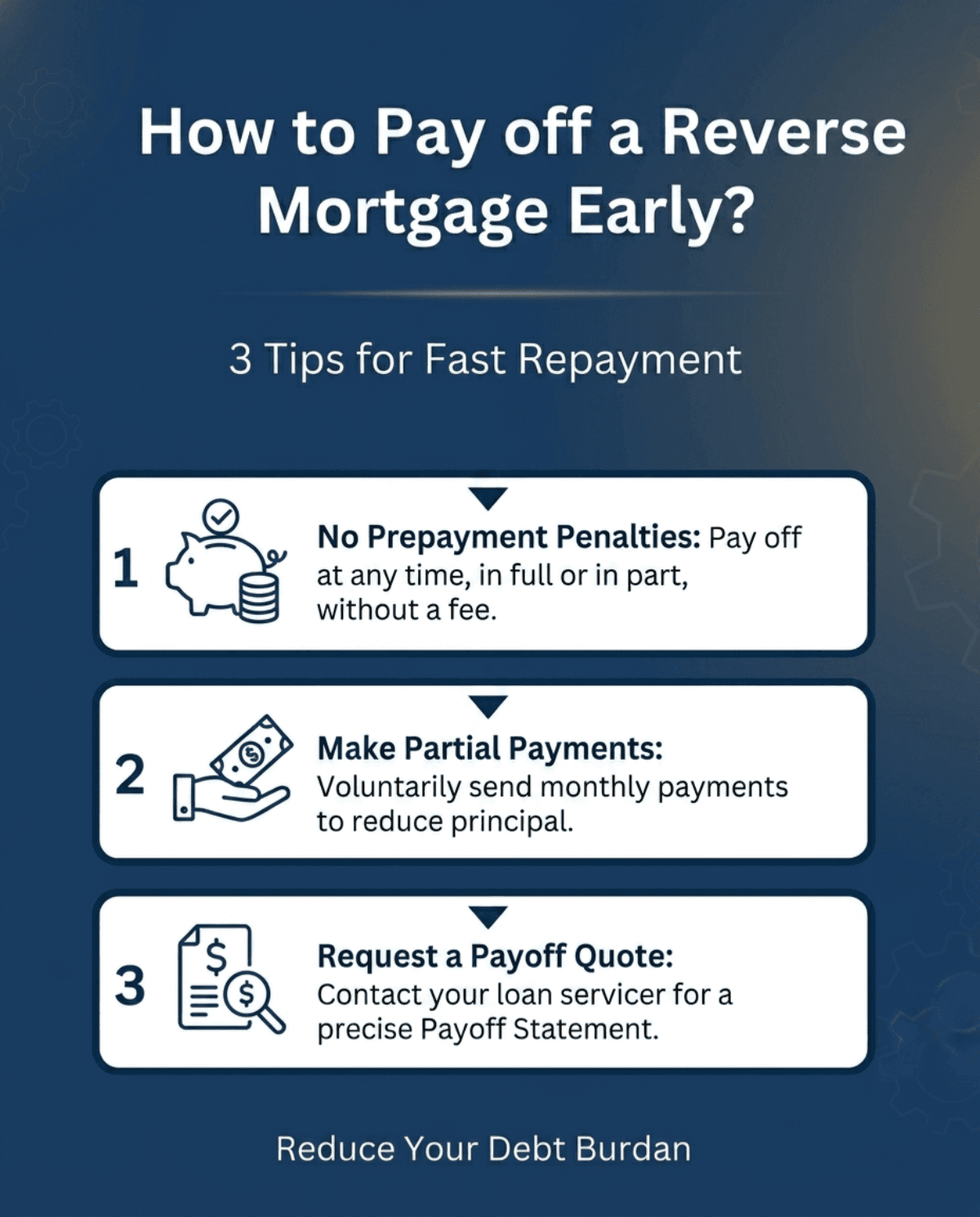

How to Pay off a Reverse Mortgage Early?

If your goal is to reduce the debt burden over time without fully exiting the program, you absolutely can pay it off early. Many people assume they are locked in, but that's a myth. Here are my top tips for fast repayment:

-

No prepayment penalties: Federal law prohibits lenders from charging you a fee for paying off a HECM early. You may repay the reverse mortgage in full or in part at any time, generally without a prepayment penalty.

-

Make partial payments: You don't need a lump sum. Voluntarily sending monthly payments reduces your principal, which drastically slows down the aggressive compounding interest.

-

Request a payoff quote: Always contact your loan servicer directly to request an official "Payoff Statement." Because interest accrues daily, the exact amount you owe changes constantly. You need this precise figure before wiring any funds.

FAQs About Paying Back a Reverse Mortgage

Q1. Can you pay back a reverse mortgage monthly?

Yes, absolutely. While the reverse mortgage lender never requires you to make monthly payments, you are entirely free to do so voluntarily. Making regular contributions toward the principal and interest is a smart strategy I often recommend. It effectively stops the loan balance from ballooning out of control and preserves more equity for your estate.

Q2. How long do you have to pay back a reverse mortgage after death?

Typically, heirs have exactly 6 months from the borrower's passing to settle the debt. However, if you are actively trying to sell the property or secure financing, you can contact the servicer to request up to two 90-day extensions. With HUD approval, this gives families a maximum of 12 months to finalize everything.

Q3. What happens if you inherit a house with a reverse mortgage?

You have three primary choices: repay the loan to keep the house, sell the property to pocket any remaining equity, or hand the deed back to the lender. Thanks to the non-recourse clause, if the house is underwater, you are never legally required to pay the difference out of your own pocket.

Q4. Who pays the reverse mortgage when the owner dies?

The reverse mortgage is paid off either by the proceeds from selling the property itself, or by the heirs if they choose to keep the home. Heirs are generally not personally liable for any shortfall on a HECM, but they must pay the debt in full if they want to keep the property.

Q5. What are the heirs' responsibilities in a reverse mortgage?

Heirs must notify the loan servicer within 30 days of the borrower's passing and provide a certified death certificate. Furthermore, until the home is officially sold or handed over, the estate remains entirely responsible for maintaining the property, paying local property taxes, and keeping the homeowners insurance policy active.

Final Word

Paying back a reverse mortgage doesn't mean you have to drain your family's life savings. Choosing the right path simply depends on your home's current equity and your long-term goals.

Based on my experience, here is how I usually break it down:

-

If your home has high equity: Sell the property on the open market, satisfy the lender, and keep the leftover profit.

-

If you want to keep a legacy home: Pay with cash or secure a new traditional mortgage, taking full advantage of the HUD 95% rule if the home is underwater.

-

If the property is severely underwater: Execute a Deed in Lieu of Foreclosure to walk away without stress.

If you are currently facing a maturity event, your very first step should be contacting your loan servicer for an official payoff statement or consulting a financial advisor.