What is a Residential Bridge Loan? Features, Pros & Cons

If you've ever found your dream home before putting a "For Sale" sign on your current one, you know the panic that sets in. I've seen countless buyers lose out on perfect properties simply because their equity was locked away in their old house. This is where a Residential Bridge Loan comes in.

Many people confuse these with commercial bridge loans used for massive apartment complexes, but the residential version is a different beast entirely. It's a short-term tool designed specifically for homeowners like you. In this guide, I'll break down how these loans work and why I often suggest using Bluerate to find a local expert who can help you bridge that financial gap without the stress.

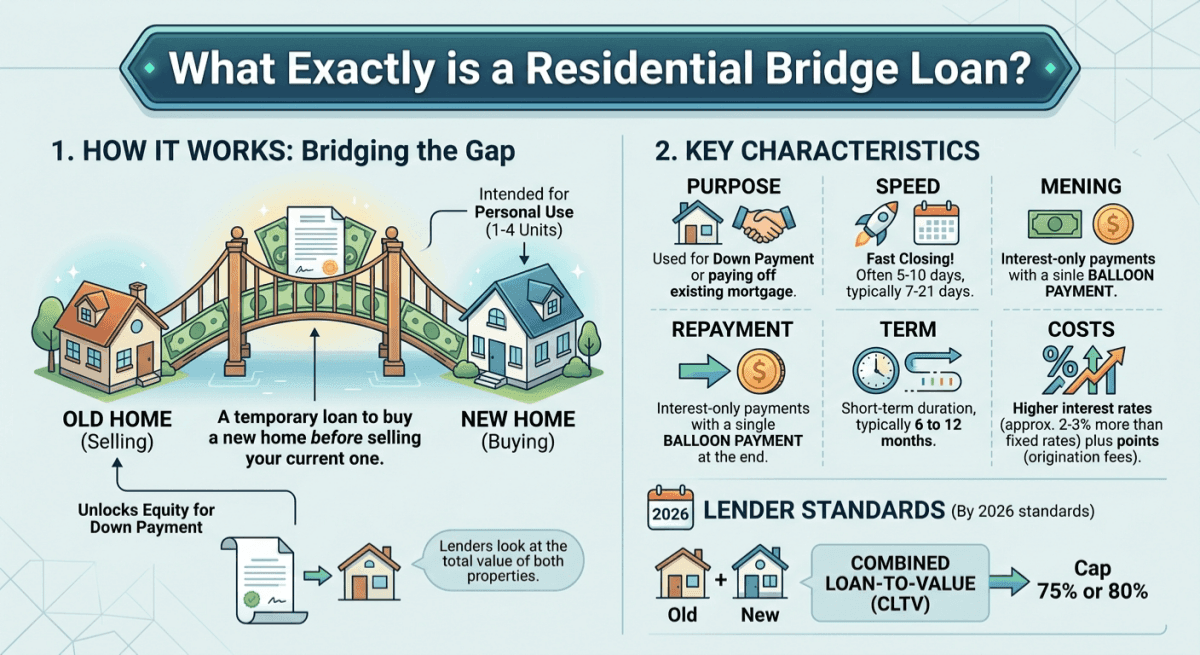

What Exactly is a Residential Bridge Loan?

To understand this, we first need to distinguish it from its commercial cousin. While commercial bridge loans fund business ventures or large-scale developments, a Residential Bridge Loan is strictly for 1-4 unit properties intended for personal use. Think of it as a temporary financial "bridge" that spans the gap between the purchase of a new home and the sale of your existing one.

From my experience, these loans carry a very specific set of features:

- Purpose: Primarily used to fund a down payment or "buy out" the existing mortgage on your current home.

- Speed: Unlike a traditional 30-year mortgage that takes 30-45 days, residential bridge loans can often close in as few as 5-10 days for simple cases, though full closing typically ranges from 7-21 days depending on appraisals and underwriting.

- Repayment: Most are "interest-only" loans with a balloon payment at the end. They usually have a term of 6 to 12 months.

- Costs: Expect interest rates to be 2% to 3% higher than standard fixed rates, plus 1-2 "points" (origination fees).

By 2026 standards, lenders are increasingly looking at the combined loan-to-value (CLTV) of both properties, often capping it at 75% or 80%.

Also Read: HELOC vs Bridge Loan: What are the Differences? Full Guide

Who Should Actually Use a Bridge Loan?

I've found that bridge loans aren't for everyone, but they are a lifesaver for specific groups. The most common user is the "Move-up Buyer", someone whose family is outgrowing their current space and needs to act fast in a competitive market. In 2026, where "no-contingency" offers are often the only ones that get accepted, having a bridge loan makes you as strong as a cash buyer.

It's also an excellent fit for Downsizers, seniors who want to buy a smaller home first to make the moving process physically easier. If you're unsure if you fit the profile, I highly recommend using the Bluerate AI Agent. It's a smart assistant that helps you determine your loan eligibility based on your specific property type and matches you with a Loan Officer who understands your local market nuances.

The Honest Truth: Pros and Cons

Every financial tool has its trade-offs, and I believe in being transparent about them.

Benefits:

- Winning the Bid: You can make an offer without a "sale of home" contingency, which sellers hate.

- Peace of Mind: You only move once. You don't have to find a temporary rental while waiting for your new house to close.

- Speed: Access to capital is nearly immediate compared to traditional refinancing.

Drawbacks:

- The Cost: The interest rates are significantly higher. According to recent 2026 market data, you might see rates in the 8% to 11% range.

- Double Debt: For a few months, you are technically responsible for two loans.

- High Equity Requirement: If you don't have at least 20-30% equity in your current home, you likely won't qualify.

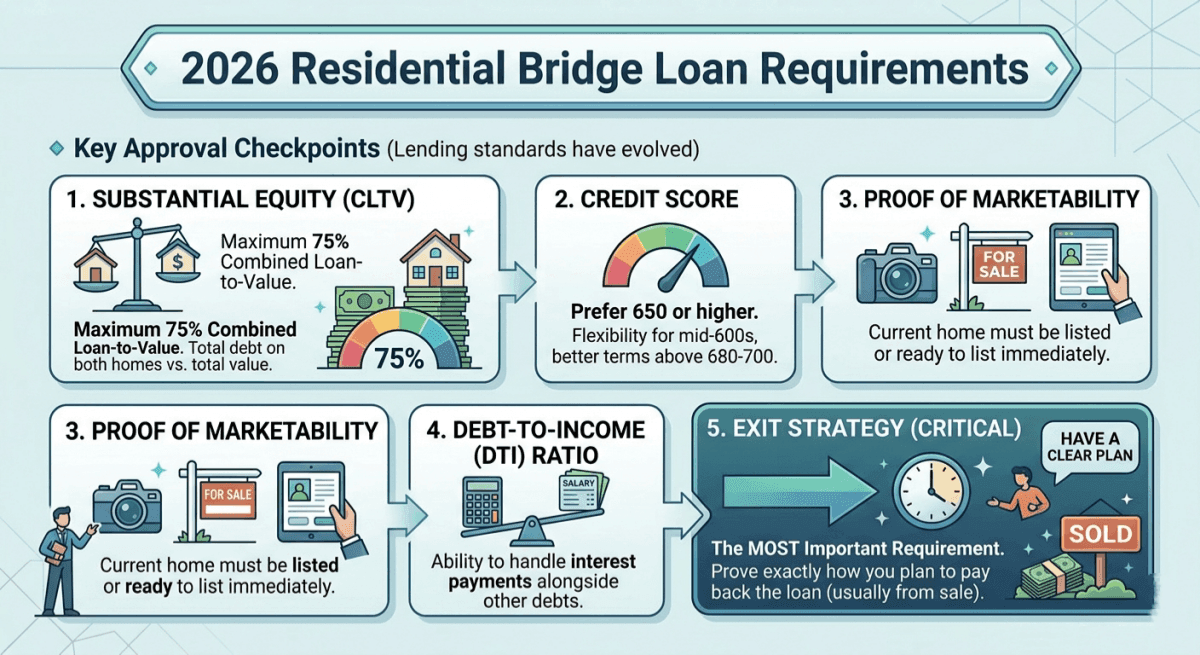

2026 Residential Bridge Loan Requirements

Lending standards have evolved. To get approved today, you typically need to check these boxes:

- Substantial Equity: Most lenders require a maximum 75% Combined Loan-to-Value (CLTV). This means the total debt on both homes shouldn't exceed 75% of their total value.

- Credit Score: While some hard money lenders are flexible (scores as low as mid-600s), most residential bridge lenders prefer a score of 650 or higher, with better terms above 680-700.

- Proof of Marketability: You'll need to show that your current home is either listed or ready to be listed immediately.

- Debt-to-Income (DTI): Even though it's short-term, lenders still want to see that you can handle the interest payments alongside your other debts.

I always tell my clients: the "Exit Strategy" is the most important requirement. You must prove exactly how you plan to pay the loan back, usually through the sale of the house.

How to Get a Residential Bridge Loan? The Smart Way

The process is faster than a standard mortgage, but it requires more precision. Here is the path I recommend:

Step 1: Calculate your equity. Use a tool or a local appraiser to see what your home is actually worth today. Step 2: Find a specialized lender. Not every big bank offers bridge loans. This is where Bluerate shines. Instead of calling dozens of banks, you can use the Bluerate platform to search for Loan Officers in your specific zip code who specialize in bridge or "Non-QM" lending. Step 3: Compare "Real" Rates. Don't just look at the interest rate. Look at the mortgage points and closing costs. Step 4: Get Pre-Approved. In today's market, you need that letter in hand before you tour a home.

Bluerate makes this incredibly easy. It's a transparent marketplace that bridges the gap between you and the mortgage experts, letting you compare quotes from over 100 lenders without your data being sold to a hundred different telemarketers.

FAQs About Residential Bridge Loans

Q1: Is a Bridge Loan better than a HELOC?

A HELOC is cheaper if you already have it in place. However, most lenders won't let you open a new HELOC if your home is already listed for sale. In that case, a bridge loan is your only option.

Q2: How long does approval take?

Usually between 7 and 14 days, though some tech-forward lenders on Bluerate can move even faster if your documentation is ready.

Q3: Can I use a bridge loan for a fixer-upper?

Yes, though that often crosses into "Fix and Flip" territory. Ensure you specify your intent to your Loan Officer so they can match you with the right product.

Q4: What happens if my house doesn't sell in 6 months?

Most bridge loan lenders offer an option to extend for a fee, but it's vital to have a "Plan B," such as lowering your asking price to ensure a quick exit.

Final Word

A Residential Bridge Loan is the ultimate "safety net" for homeowners navigating a fast-moving real estate market. It removes the "contingency" barrier and gives you the leverage of a cash buyer. However, because of the higher costs and shorter terms, you shouldn't go it alone.

This is exactly why Bluerate create a more intuitive, transparent way for you to find the right person for the job. Whether you use their AI Agent for a quick match or browse their directory of trusted Loan Officers, the goal is to give you back control. Don't let your dream home slip away just because your money is stuck in your current walls. Visit Bluerate.ai and find your bridge today.

People Also Read

- Best Bridge Loan Lenders for Homebuyers and Investors

- Guide: How to Get a Prequalification for a Mortgage?

- 3 Methods: How to Calculate Debt-to-Income Ratio for Mortgage?

- Cash-out Refinance vs HELOC: All Differences to Learn

- Step-By-Step Guide: How to Refinance a Mortgage Loan?

- Zeitro Strata Review: World's No.1 Best Mortgage Guidelines Checker