2026 Guide: How to Get a Prequalification for a Mortgage?

In my years as a mortgage advisor, the most common question I hear from eager house hunters is, "How do I actually get a mortgage prequalification?" Figuring out where to borrow money, and how much you can afford, often brings more anxiety than excitement.

But here we are in 2026, and the old way of driving to a bank or dodging relentless telemarketers is dead. Today, securing that initial estimate is something you can safely do right from your couch using smart online platforms like Bluerate. Let's walk through exactly how to get started.

What is Mortgage Prequalification?

Think of a mortgage prequalification as a rough sketch of your buying power. It's an initial estimate from a lender showing how much money you might be eligible to borrow, based entirely on the financial details you provide upfront. You tell them your income, savings, and monthly debts. In return, they run a "soft pull" on your credit profile. I always reassure my nervous buyers: a soft pull won't drop your credit score by a single point.

If the numbers align, the lender hands you a mortgage prequalification letter. This document is basically your ticket to start window-shopping. It tells real estate agents you have a realistic budget and aren't just browsing for fun.

How to Get Prequalified for a Mortgage: A Step-by-Step Guide for First-Time Buyers

If you are a first-time homebuyer, stepping into the financial side of real estate feels daunting. I get it. But grabbing this initial letter is genuinely a quick process. We just need to tackle four straightforward steps: checking your credit, gathering some basic numbers, finding a reliable loan officer online, and waiting for the official letter. Here is how it works.

STEP 1. Check Credit Score & Report

Long before you let a professional look at your profile, you need to know exactly what they will see. Your credit score acts as the gatekeeper to the best loan types and lowest interest rates. I've had clients shocked by sudden rate hikes, only to discover a tiny, unpaid medical bill dragging their score down.

Go to AnnualCreditReport.com to grab your free weekly file. Scanning your own record counts as a soft inquiry, so don't worry about hurting your score. Take ten minutes to comb through the data. If you spot glaring errors, like an account you closed years ago showing up as delinquent, dispute it immediately. Having a clean slate before a lender does their own check puts you in a much stronger negotiating position.

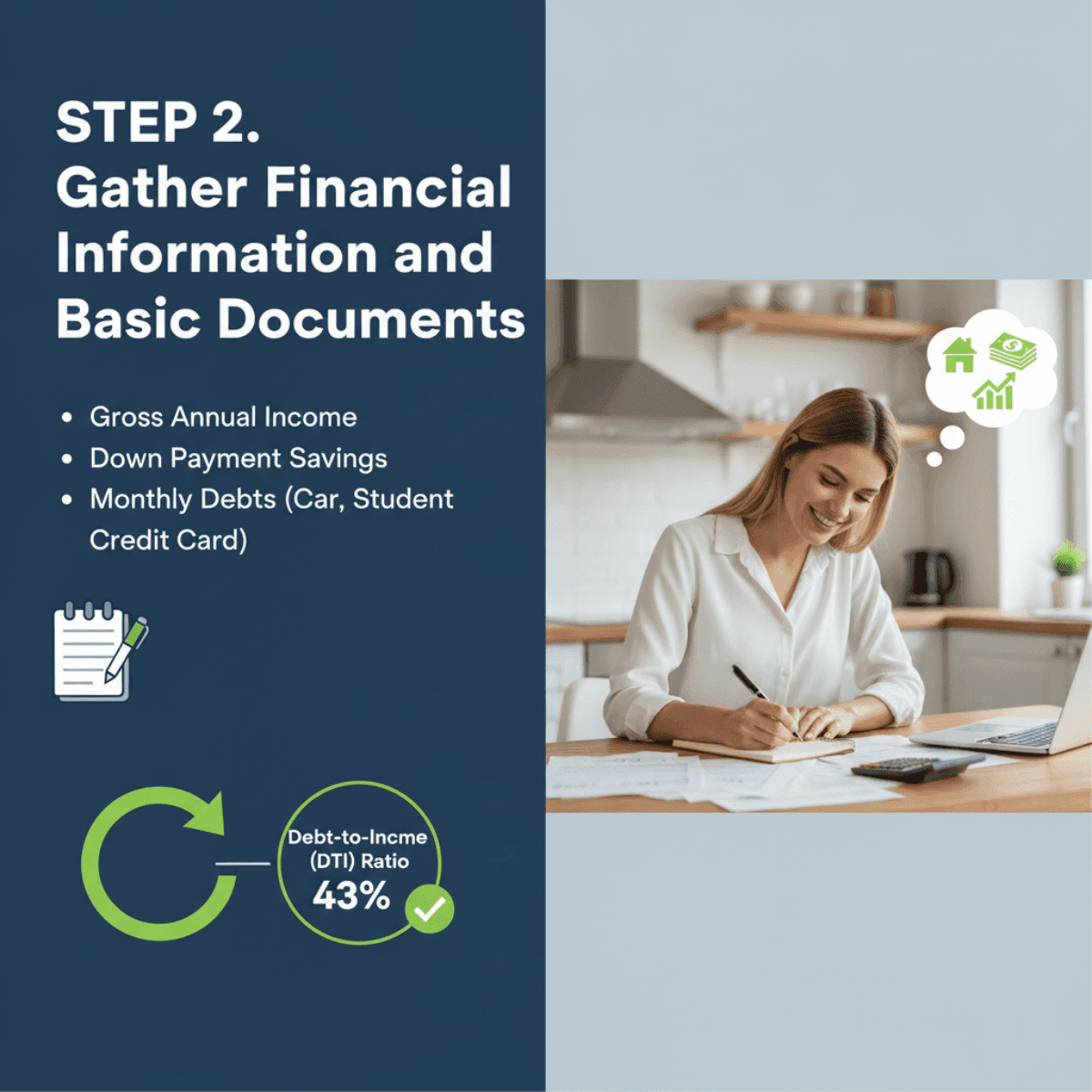

STEP 2. Gather Financial Information and Basic Documents

Because getting prequalified relies on self-reported data rather than hard proof, you won't be asked to upload massive PDF files of W-2s or bank statements just yet. However, guessing your salary is a terrible idea. If you overestimate your earnings now, your actual loan application will crash later.

Grab a notepad and jot down three honest figures: your gross annual income (before taxes), the total cash available for a down payment, and your monthly recurring debt. I'm talking about car payments, student loans, and credit card minimums, not groceries or Netflix subscriptions. Lenders compare your debt against your income to find your Debt-to-Income (DTI) ratio. From my daily experience, keeping that DTI under 43% gives you the best shot at a smooth approval process.

Also Read: 3 Methods: How to Calculate Debt-to-Income Ratio for Mortgage?

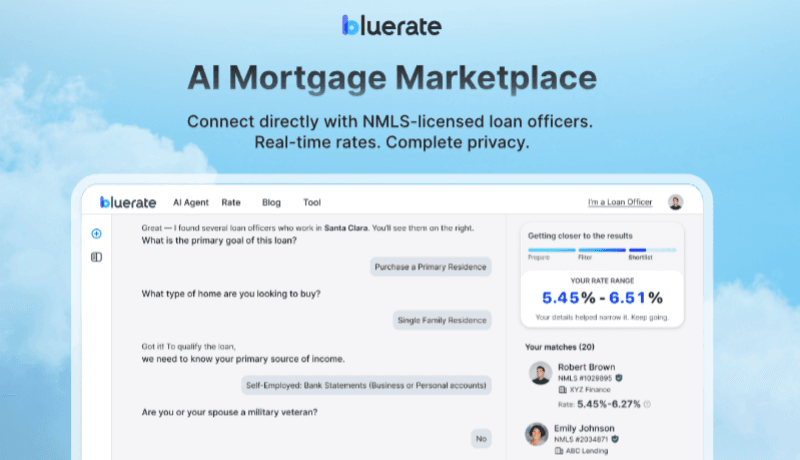

STEP 3. Find the Right Loan Officer and Apply Online

Finding a trustworthy mortgage professional used to be a nightmare. Borrowers would fill out a generic web form and instantly get bombarded by fifty aggressive sales calls. Thankfully, the industry has evolved. My top recommendation for avoiding that trap is using a modern marketplace like Bluerate to handle the matching securely.

Instead of selling your data to the highest bidder, Bluerate acts as a bridge. You stay completely anonymous while browsing personalized, verified rates from over 100 lenders. There are no fake "teaser" numbers here.

What really makes it stand out is the Smart AI Agent. You can just open a chat, and this 24/7 virtual assistant asks a few basic questions to calculate your DTI. It's perfect if you feel intimidated asking a human "how much down payment do I actually need?" Based on your answers, the AI precisely matches you with top-rated, NMLS-licensed loan officers in your specific ZIP code.

Whether you are buying a single-family home, a condo, or you're a self-employed buyer needing a specialized Non-QM expert, the platform handles it all. You pick the professional you want to work with on your own terms. It's an all-in-one hub that genuinely respects a "privacy first" approach, letting you bypass the spam and move toward a prequalification about two and a half times faster than the old-school route.

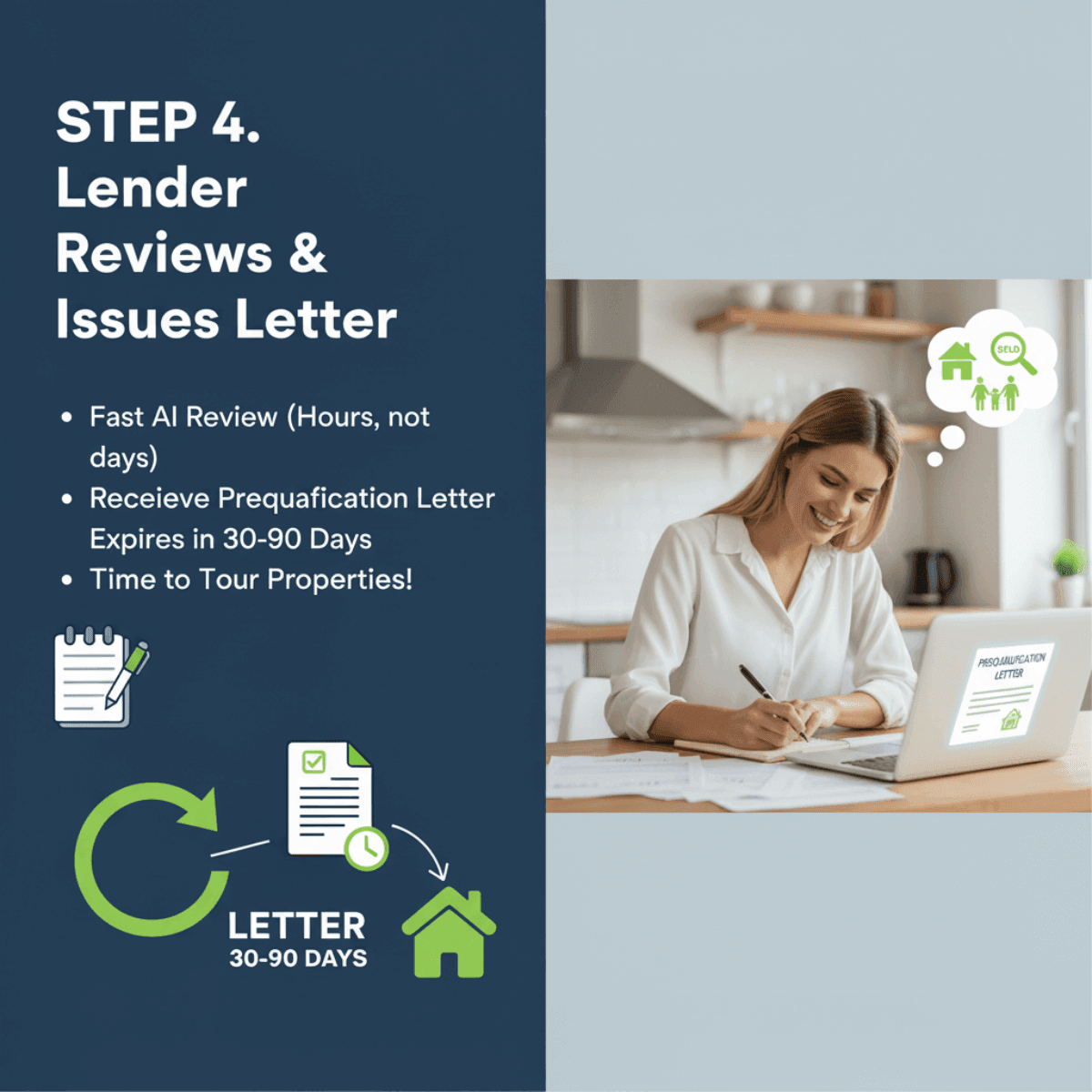

STEP 4. Lender Reviews & Issues Letter

After you connect with your chosen loan officer and share those basic financial details, the hard part is over. Thanks to AI analysis speeding up the backend work, lenders evaluate these initial profiles incredibly fast. You won't be sitting around for a week waiting for a phone call. It often takes just a few hours.

If your numbers meet the baseline guidelines, the lender generates your prequalification letter. Keep in mind that this document comes with an expiration date, usually between 30 and 90 days. The housing market moves fast, and lenders know financial situations change. If you haven't found the right house before the letter expires, don't panic. Just text your loan officer for a quick update. Now, call your real estate agent. You are ready to start touring properties.

Also Read:

- Best Mortgage Lenders for Low-Income: Top-rated Picks

- Best Foreign National Mortgage Lenders: How to Choose?

- Best Mortgage Lenders for Self-Employed: Top-Rated Picks

- Best DSCR Lenders Near Me: Highlights, Pros & Cons

- 8 Best Non-QM Mortgage Lenders: Get Your Best Pick Here

Bonus Tips for You to Get a Prequalification

Want to make sure this phase goes off without a hitch? Here are a few insider strategies I constantly share with my buyers:

-

Shop Around: Never accept the very first rate you are handed. Different lenders carry different margins. Use a platform like Bluerate to instantly view live rates across 30+ institutions. Doing this early on gives you a realistic benchmark without damaging your credit.

-

Keep Finances Stable: This is the biggest rookie mistake. Once you start the mortgage process, freeze your spending habits. Do not open a new store credit card to buy furniture, and absolutely do not finance a new car. Taking on new debt immediately alters your DTI ratio and can tear up your prequalification overnight.

-

Leverage AI Tools: Don't be afraid to lean on tech. If you are just curious about your borrowing power, or perhaps looking into a refinance later on, chat with the Bluerate AI Agent. It is an amazing way to get unbiased, professional answers to your specific financial questions without triggering a flood of annoying texts from a commissioned salesperson.

FAQs About Getting a Prequalification for Mortgage

Q1. How hard is it to get prequalified for a mortgage?

It is incredibly easy. Because it relies on self-reported estimates rather than verified documents, you can complete the whole process online in just a few minutes.

Q2. What is needed to pre-qualify for a mortgage?

You simply need a rough estimate of your annual income, your total monthly debt payments, your available down payment funds, and permission for the lender to do a soft credit check.

Q3. What is the difference between pre-qualification and preapproval?

Prequalification is step one: an unverified estimate using a soft credit pull. Preapproval is step two: a serious commitment where the lender does a hard credit pull and verifies your actual tax returns and bank statements. Sellers take preapprovals much more seriously.

Also Read:

- Guide: How to Prequalify for a Mortgage Loan Online?

- A Detailed Guide: How to Get Preapproved for a Mortgage?

Q4. Can I get a prequalification for a mortgage online?

Yes, it is the standard way to do it in 2026. You can safely get prequalified from your smartphone using secure platforms like Bluerate.ai, skipping the traditional bank lobby entirely.

Final Word

Securing a prequalification is the first real milestone in your homeownership journey. It shifts you from a dreamer looking at real estate apps into a legitimate buyer with a defined budget. I always tell my clients that finding out your borrowing power shouldn't involve stress, piles of paperwork, or fending off telemarketers.

If you are ready to take that first step privately and efficiently, head over to Bluerate.ai. Just click the "Chat with AI" button on their homepage. Have a quick, zero-pressure conversation with the virtual assistant, find a top-tier local loan officer, and get your mortgage prequalification today so you can finally go find your home.