Best No-Doc Mortgage Loans in 2026: Everything You Need to Know

I know firsthand how frustrating the traditional mortgage process can be if you don't fit the standard W-2 mold. As a freelancer or business owner, handing over endless tax returns and still getting rejected by traditional mortgage lenders feels defeating. That's exactly where no-doc mortgage loans come in as a lifesaver.

These alternative documentation solutions let you qualify based on real-world cash flow rather than rigid tax papers. Navigating alternative documentation loans can be tricky, which is why matching with a local, top-rated loan officer for a free consultation on Bluerate.ai is the smartest first step to take.

Key Takeaways

- Modern no-doc loans are actually "Alt-Doc" or Non-QM loans. True blind approvals no longer exist in the 2026 market.

- Perfect for non-traditional earners like self-employed professionals, freelancers, and real estate investors.

- No tax returns required, but lenders will verify your cash flow or liquid assets.

- Expect trade-offs: You'll likely face higher interest rates and need a larger down payment (typically 20% or more).

What is a No-Doc Mortgage Loan?

A no-doc mortgage, short for a no-documentation loan, allows borrowers to secure home financing without handing over traditional income proofs like W-2s, pay stubs, or tax returns.

Before the 2008 financial crisis, these were notoriously known as NINJA loans (No Income, No Job, No Assets). Lenders basically took borrowers at their word, which led to widespread defaults. Today, thanks to the Dodd-Frank Act and the Consumer Financial Protection Bureau's Ability-to-Repay (ATR) rule, those pure blind-approval loans are legally extinct for primary residences.

In 2026, when we say "no-doc," we are actually talking about Non-QM (Non-Qualified Mortgage) or Alt-Doc (Alternative Documentation) loans. Lenders still verify your ability to repay, just through non-traditional metrics.

Main features include:

- Alternative verifications: Focuses on bank deposits, liquid assets, or property cash flow rather than tax returns.

- Faster processing: Less paperwork often translates to a quicker underwriting phase.

- High flexibility: Tailored for complex financial situations where standard metrics fail to show a borrower's true purchasing power.

Also Read: Best No-Doc Mortgage Lenders: Pick the Right One

How Does a No-Doc Mortgage Work?

If a lender isn't looking at your W-2s or tax returns, how do they know you can afford the monthly payments? The process works by shifting the focus from taxable income to your actual, liquid cash flow or real estate performance.

Here is how underwriters evaluate your application today:

- Bank Statements: Lenders will analyze 12 to 24 months of your personal or business bank statements to calculate a monthly average of your incoming deposits.

- Asset Depletion: If you have substantial wealth, lenders divide your total liquid assets by a specific term (often 60 to 360 months) to generate a qualifying "monthly income."

- Property Cash Flow (DSCR): For investment properties, the lender looks strictly at the projected rental income. If the rent covers the mortgage, your personal income isn't even factored in.

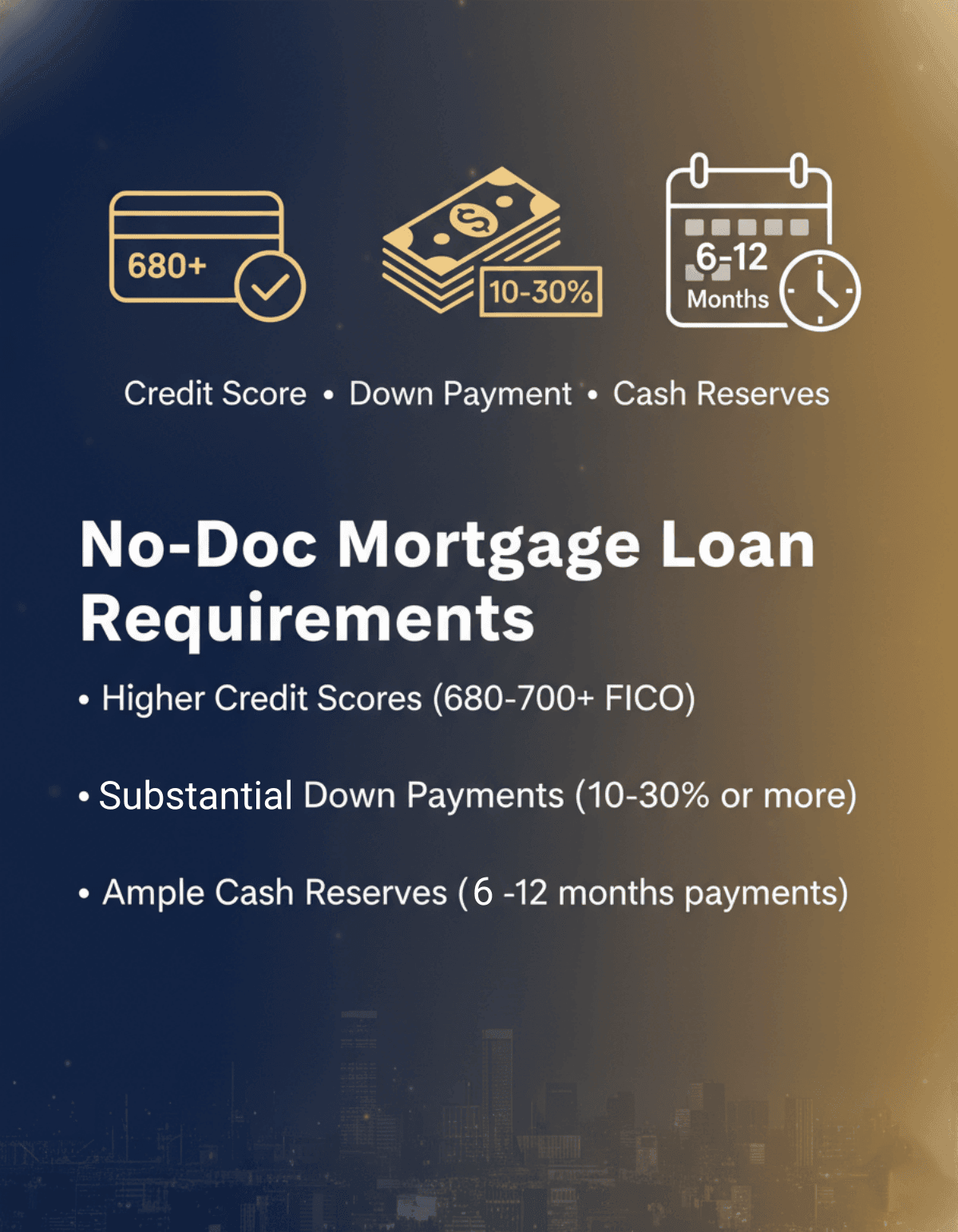

No-Doc Mortgage Requirements

I always remind my clients: bypassing standard paperwork does not mean bypassing lending standards. To offset the higher risk they take on by skipping tax returns, banks enforce stricter financial buffers.

To qualify in the 2026 market, you generally need to meet these core requirements:

- Higher Credit Scores: You'll typically need a FICO score of 680 to 700+. While some non-QM lenders accept lower scores, it usually triggers massive penalties in your loan terms.

- Substantial Down Payments: Forget the standard 3% or 5%. Expect to put down 10% to 30% or more, depending on the program and your profile.

- Ample Cash Reserves: Most underwriters want to see enough liquid cash in your account to cover 6 to 12 months of mortgage payments, proving you can handle financial dry spells.

Pros and Cons of No-Doc Verification Mortgage

Opting for a non-traditional home loan is a strategic move, but it comes with distinct trade-offs. Here is an objective look at the advantages and disadvantages before you sign on the dotted line.

Benefits of No-Doc Verification Mortgage

- Protects privacy & saves time: You don't have to dig up years of complex tax returns or explain heavy business write-offs.

- Accommodates complex earners: Ideal for those with multiple income streams, gig workers, or seasonal business owners.

- Faster closing: Fewer documents to verify can mean less back-and-forth with loan processors.

Drawbacks of No-Doc Verification Mortgage

- Steeper Interest Rates: You will almost always pay a premium, usually 1% to 2% higher than conventional prime rates.

- Large upfront costs: The mandatory 20%+ down payment prices out many average buyers.

- Limited availability: Not all mainstream banks offer them, meaning you'll likely need to work with specialized mortgage brokers.

Who Should Consider a No-Doc Mortgage?

Standard mortgages are designed for W-2 employees with predictable paychecks. If you don't fit that box, alternative documentation loans are built specifically for you.

You should strongly consider a no-doc or Non-QM loan if you fall into one of these categories:

- Self-Employed Professionals & Freelancers: Your CPA works hard to maximize your deductions, which legally lowers your taxable income but makes you look "poor" on paper to traditional banks.

- Real Estate Investors: You want to scale your portfolio quickly without your personal debt-to-income (DTI) ratio holding you back.

- High-Net-Worth Individuals: You might be retired or taking a sabbatical, meaning you lack a steady monthly paycheck but have millions in liquid assets readily available.

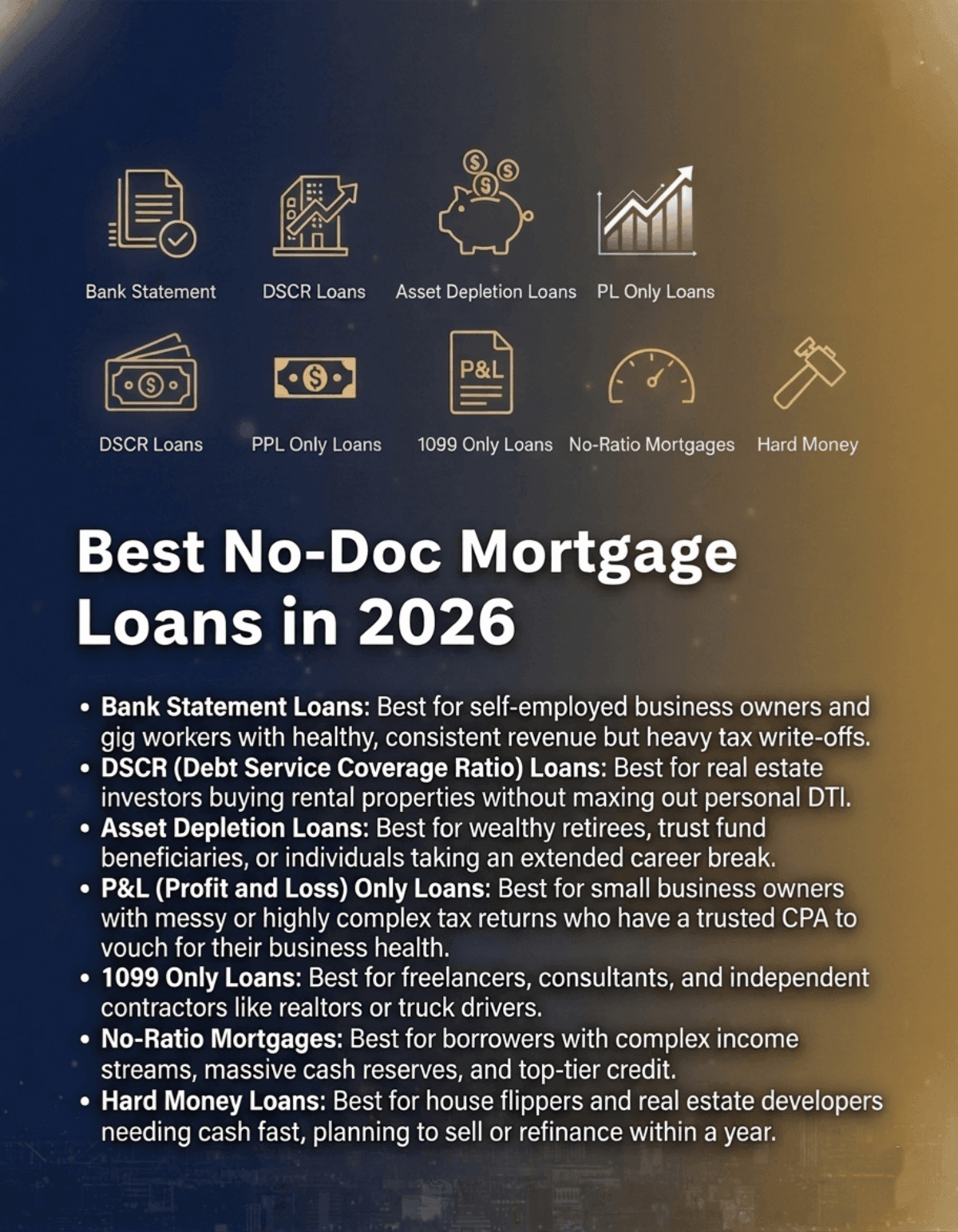

Best No-Doc Mortgage Loans in 2026

Depending on your exact financial scenario, there is a specialized Non-QM product ready to help you secure funding. Let's break down the best alternative documentation loans currently dominating the 2026 market.

1. Bank Statement Loans

Instead of looking at your tax returns, lenders calculate your qualifying income by averaging the gross deposits into your personal or business accounts over the last 12 to 24 months. It's an incredibly practical way to show your true cash flow.

- Best for: Self-employed business owners and gig workers who have healthy, consistent revenue but claim heavy tax write-offs.

2. DSCR (Debt Service Coverage Ratio) Loans

This is the ultimate tool for property investors. Your personal income and employment history are completely ignored. Instead, the lender checks if the property's gross rental income covers the monthly mortgage obligation. If the ratio is 1.0 to 1.25 or higher, you're usually good to go with DSCR loans.

- Best for: Real estate investors looking to buy rental properties without maxing out their personal DTI.

Also Read:

- DSCR Loan Requirements: Ratio, Credit Score, Down Payment, Type

- DSCR Loan Pros and Cons: Is It the Right Strategy for Your Investment?

- DSCR Formula: How to Calculate DSCR in Real Estate?

- Best DSCR Lenders Near Me: Highlights, Pros & Cons

- Full Guide: How to Get a DSCR Loan? Everything Here

3. Asset Depletion Loans

If you have significant wealth but no traditional job, lenders can utilize your liquid assets, like savings, stocks, and retirement accounts, to manufacture a monthly income. For instance, they might divide your $2 million portfolio by 120 months, giving you a qualifying "income" of over $16,000 a month.

- Best for: Wealthy retirees, trust fund beneficiaries, or individuals taking an extended career break.

Also Read:

- Detailed Guide on Asset Depletion Loan: Definition, Pros & Cons

- Best Asset Depletion Lenders: Top Rank Here

4. P&L (Profit and Loss) Only Loans

You simply submit a Profit and Loss statement prepared by a licensed CPA or tax professional. The underwriter uses the net income shown on this single document to qualify you, entirely skipping the need for official IRS tax transcripts.

- Best for: Small business owners with messy or highly complex tax returns who have a trusted CPA to vouch for their business health.

5. 1099 Only Loans

If you work as an independent contractor, you probably receive 1099 forms instead of a W-2. With this loan, the lender looks strictly at your 1099 earnings from the past year or two. They usually apply an assumed expense ratio to figure out your net income without digging into your actual business receipts.

- Best for: Freelancers, consultants, and independent contractors, like realtors or truck drivers.

6. No-Ratio Mortgages

This is one of the closest things left to a true pre-2008 no-doc loan. The lender does not calculate your Debt-to-Income (DTI) ratio at all. Because they are taking a massive leap of faith, you must offset their risk with an incredibly high down payment and an immaculate credit history.

- Best for: Borrowers with complex, hard-to-prove income streams who happen to have massive cash reserves and top-tier credit.

7. Hard Money Loans

These are short-term, asset-based loans provided by private investors rather than traditional banks. They care almost exclusively about the property's potential rather than your personal income. The approval is blazing fast, but you'll pay exorbitant interest rates and fees.

- Best for: House flippers and real estate developers who need cash fast and plan to sell or refinance within a year.

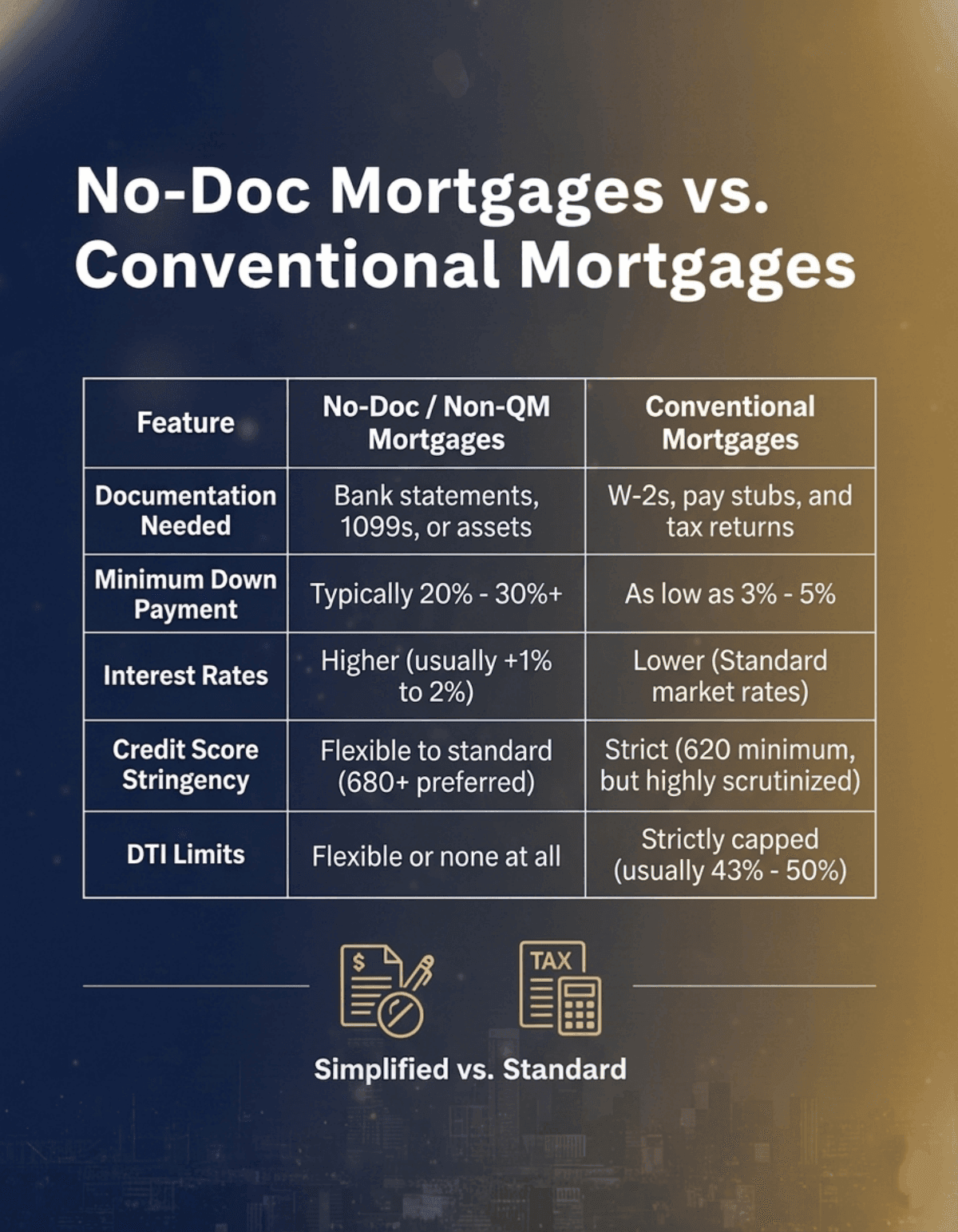

No-Doc Mortgages vs. Conventional Mortgages

When deciding between a traditional loan and an alternative route, it all comes down to what you can comfortably prove on paper versus what you can afford in real life. Conventional mortgages are heavily regulated by Fannie Mae and Freddie Mac, offering the lowest rates but demanding the most rigid paperwork. Non-QM loans cut the red tape but charge you for the convenience.

Here is a quick breakdown of how they compare in today's market:

FAQs About No-Doc Mortgage Loans

Q1. Are no doc loans hard to get?

No, they aren't inherently hard to get if you have strong financials, like a hefty down payment and a good credit score. The actual challenge is finding the right lender, as standard commercial banks don't offer these Non-QM products. Working with a specialized broker is key.

Q2. What credit score is needed for a no-doc loan?

You generally need a FICO score of 680 to 700 or higher to secure favorable terms. While some niche lenders might accept a score as low as 620, you should expect significantly steeper interest rates and much larger down payment requirements in return.

Q3. How much can I borrow with a no-doc loan?

Borrowing limits depend heavily on your property value and available assets. Non-QM loans often cater to the luxury market, so it's quite common to see approvals ranging from a few hundred thousand up to several million dollars for alternative Jumbo loans.

Q4. Can I get a no-doc loan for a primary residence?

Yes, you absolutely can. Options like Bank Statement loans and Asset Depletion loans are frequently used by self-employed buyers to purchase primary homes. However, DSCR loans are strictly reserved for investment properties and cannot be used for a house you plan to live in.

Q5. Is there still no-doc mortgage loan available?

Yes, but they exist primarily as Non-QM (Non-Qualified Mortgage) or Alt-Doc loans to comply with modern federal regulations. You won't find the blind-approval NINJA loans from 2008, but you can still completely bypass the need for traditional W-2s and tax returns.

Q6. How long does it take to get approved for a no-doc loan?

Because there is far less paperwork to verify, the underwriting process is often faster. You can typically expect approval within 2 to 4 weeks. If you are utilizing a Hard Money loan, the turnaround time can be as quick as a few days.

Final Word: Should You Get a No-Doc Mortgage?

If your lack of a traditional W-2 has been the only thing standing between you and your dream home or next investment property, a Non-QM loan is an incredibly powerful tool. You don't have to let a complex tax return dictate your purchasing power. Yes, you will need to bring a larger down payment and accept a slightly higher rate, but for many self-employed individuals and investors, the freedom and flexibility are well worth the cost.

Finding a reliable lender offering competitive no-doc mortgage rates doesn't have to be overwhelming. At Bluerate, we connect you with top-tier, localized loan officers who specialize in alternative documentation loans. Get a free consultation today and discover the best financing path for your unique financial situation.